When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

Evo GeneralDiscuss any generalized technical Evo related topics that may not fit into the other forums.

Please do not post tech and rumor threads here.

Sponsored by: RavSpec - JDM Wheels Central

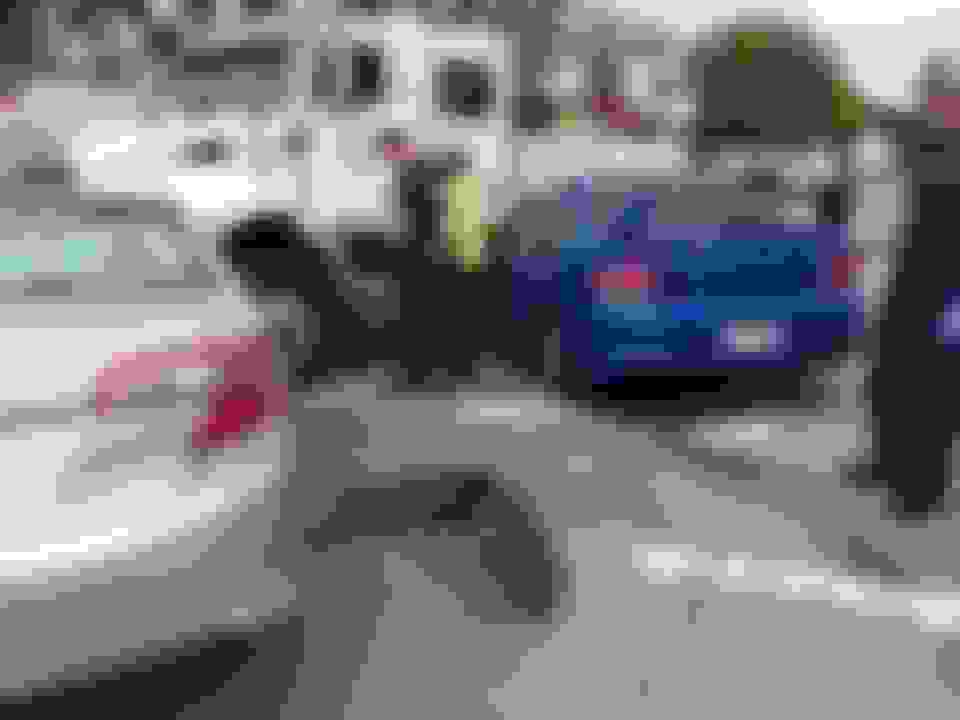

Bought this car from a member on here not too long ago after searching for 2 years. It was a mostly stock Blue by you with 55k miles in awesome condition. Couple days ago, some dumb lady decided she didn't want to yield and wrecked my car as I was going through a green light.

This was my first accident and first time dealing with insurance, so I had some questions. My car books for 13k; however, I couldn't find one in similar condition as mine for under $18000 anywhere also given the rare color. Anyone know what I'm to expect? Any advice would be helpful. If it helps any, I'm insured with State Farm and the dumb ***** didn't have insurance.

All I want is an exact replacement of what was lost and $13k won't cut it. That'd get me a 135k mile evo in fair condition.

Last edited by MitsuRishi; Mar 31, 2016 at 08:37 PM.

Being a city vehicle I am sure your insurance company will get their money back. I have had 3 totals in my life and have been fairly satisfied in all instances. Obviously I can't say that will be your case but they will come to you with the buyout price and you can take it from there whether you agree to it or not.

P.S. Terrible to see and I know I would feel like I lost a family member if it had happened to my X. And I almost forgot glad to hear that everyone involved is okay.

Last edited by CaTaSTrophiK; Mar 31, 2016 at 09:42 PM.

First of all, collect as much evidence as you can. Witnesses, photos, dash cam videos, they all help greatly in proving that the other party is at fault.

Then, I would hit up my most trusted lawyer, and if he doesn't practise in this area, I would ask him to recommend one of his alumni who does. This is just to touch base and lay down some ground work for a fantastic court case.

You should understand if the other party is at fault, how much she is liable has nothing to do with any "book value" of a Mitsubishi Lancer Evolution of same model year. It only matters how much your exact car is worth in the market.

With a fantastic court case being prepared, I would be confident in spending ~$18k out of my own pocket right now to buy another Evo of similar great condition. If money is an issue, then there is no choice other than saving up for now and waiting for the saving to reach $18k, or for the court case to eventually settle, which ever comes first.

Last, I just want to ask a few questions to make sure we are on the same page:

1) Do you have collision coverage with State Farm?

2) Do you have ANY evidence at all that proves it's other party's fault?

3) Did you snap a picture of the other driver's license or write her licence info down (so you actually know whom to sue, instead of having to ask investigators for help)?

First of all, collect as much evidence as you can. Witnesses, photos, dash cam videos, they all help greatly in proving that the other party is at fault.

Then, I would hit up my most trusted lawyer, and if he doesn't practise in this area, I would ask him to recommend one of his alumni who does. This is just to touch base and lay down some ground work for a fantastic court case.

You should understand if the other party is at fault, how much she is liable has nothing to do with any "book value" of a Mitsubishi Lancer Evolution of same model year. It only matters how much your exact car is worth in the market.

With a fantastic court case being prepared, I would be confident in spending ~$18k out of my own pocket right now to buy another Evo of similar great condition. If money is an issue, then there is no choice other than saving up for now and waiting for the saving to reach $18k, or for the court case to eventually settle, which ever comes first.

Last, I just want to ask a few questions to make sure we are on the same page:

1) Do you have collision coverage with State Farm?

2) Do you have ANY evidence at all that proves it's other party's fault?

3) Did you snap a picture of the other driver's license or write her licence info down (so you actually know whom to sue, instead of having to ask investigators for help)?

1) Yes, I have full coverage with $500 deductibles along with uninsured motorist coverage.

2) Yes, there were multiple witnesses including the 3rd party that was involved in the accident. The police report even states that she was at fault.

3) I have all her information down on the police report

Being a city vehicle I am sure your insurance company will get their money back. I have had 3 totals in my life and have been fairly satisfied in all instances. Obviously I can't say that will be your case but they will come to you with the buyout price and you can take it from there whether you agree to it or not.

P.S. Terrible to see and I know I would feel like I lost a family member if it had happened to my X. And I almost forgot glad to hear that everyone involved is okay.

The thing is, the city vehicle wasn't even at fault. It was the lady who smashed my car into them and then proceeded to smash her car into them. The police report stated she was clearly at fault. I was torn when this happened given I flew all the way out to California in September and drove it back to Houston after finding the perfect Evo.

What's done is done, I'm just hoping insurance does right and gives me enough of a payoff to replace the exact vehicle I lost. Not a beat to crap Evo with 130k miles on it.

1) Yes, I have full coverage with $500 deductibles along with uninsured motorist coverage.

2) Yes, there were multiple witnesses including the 3rd party that was involved in the accident. The police report even states that she was at fault.

3) I have all her information down on the police report

Congratz! You are on top of your life. Pay your most trusted lawyer and it should be an easy win.

Speaking of the collision coverage, it's great that you have it, but I wouldn't make a claim under it other than just letting State Farm know about the event and that I'm taking the at-fault party to the court.

This is because there are a few moving parts with collision coverage. First, it's unlikely that the claim adjuster will offer you a great deal. You might have to sue your own insurance company to get them to pay the full amount, which makes no sense to me, because suing the other party gets you the same result without increasing your future premiums. Second, if I speculate correctly, you did not have an ambulance run or even just verifiable bodily injury, did you? If you have no injury, it's unlikely that State Farm will later subrogate hard on your behalf, and thus your claim is hurting your own insurance history (the only exception is if Texas has an insurance law that makes jacking up premiums on the basis of non-at-fault accidents illegal). Typically, the premium increase might be calculated on the basis of net payout, which equals to the claim payment minus subrogation, and as a rule of thumb, your total future premium increase might be 3 to 6 times of the net payout.

Now, State Farm is a great company and usually doesn't increase your premium based on a non-at-fault accident, but in the future, any US-registered insurance company can see your collision claim and its net payout on LexisNexis CLUE database and Verisk A-PLUS database. While the exact amount is based on your state's laws and the insurance company's underwriting guidelines, this claim and net payout could hurt your insurability and premium on any insurance you buy in the future. Some companies even rate life insurance based on CLUE. It could also impact things other than insurance, such as renting a car.

Therefore, I would only file a claim under collision coverage as the last resort, such as if the other party disappears from the United States and I have no possible recourse.

Congratz! You are on top of your life. Pay your most trusted lawyer and it should be an easy win.

Speaking of the collision coverage, it's great that you have it, but I wouldn't make a claim under it other than just letting State Farm know about the event and that I'm taking the at-fault party to the court.

This is because there are a few moving parts with collision coverage. First, it's unlikely that the claim adjuster will offer you a great deal. You might have to sue your own insurance company to get them to pay the full amount, which makes no sense to me, because suing the other party gets you the same result without increasing your future premiums. Second, if I speculate correctly, you did not have an ambulance run or even just verifiable bodily injury, did you? If you have no injury, it's unlikely that State Farm will later subrogate hard on your behalf, and thus your claim is hurting your own insurance history (the only exception is if Texas has an insurance law that makes jacking up premiums on the basis of non-at-fault accidents illegal). Typically, the premium increase might be calculated on the basis of net payout, which equals to the claim payment minus subrogation, and as a rule of thumb, your total future premium increase might be 3 to 6 times of the net payout.

Now, State Farm is a great company and usually doesn't increase your premium based on a non-at-fault accident, but in the future, any US-registered insurance company can see your collision claim and its net payout on LexisNexis CLUE database and Verisk A-PLUS database. While the exact amount is based on your state's laws and the insurance company's underwriting guidelines, this claim and net payout could hurt your insurability and premium on any insurance you buy in the future. Some companies even rate life insurance based on CLUE. It could also impact things other than insurance, such as renting a car.

Therefore, I would only file a claim under collision coverage as the last resort, such as if the other party disappears from the United States and I have no possible recourse.

Thanks for the helpful advice! I didn't sustain major injuries just cuts on my arm from the airbags and some back pain; therefore, no ambulance was called for me. As far as the claims process goes, I tried to go after her insurance and apparently they told me her policy doesn't even exist in their database. My insurance also tried to go after them as well with no luck. Therefore, I proceeded with the claim under my insurance as this was my only car and I do work 2 jobs and need new transportation asap.

My insurance did tell me that once they can confirm she is at fault, my deductible will get slashed in half. The car is currently sitting at the insurance auction lot awaiting appraisal since given by my information, they deemed it a total loss. I've been told that I'll most likely get lowballed at first, but if I can prove that there are vehicles in similar condition and mileage as mine, they might adjust the payout.

Thanks for the helpful advice! I didn't sustain major injuries just cuts on my arm from the airbags and some back pain; therefore, no ambulance was called for me. As far as the claims process goes, I tried to go after her insurance and apparently they told me her policy doesn't even exist in their database. My insurance also tried to go after them as well with no luck. Therefore, I proceeded with the claim under my insurance as this was my only car and I do work 2 jobs and need new transportation asap.

My insurance did tell me that once they can confirm she is at fault, my deductible will get slashed in half. The car is currently sitting at the insurance auction lot awaiting appraisal since given by my information, they deemed it a total loss. I've been told that I'll most likely get lowballed at first, but if I can prove that there are vehicles in similar condition and mileage as mine, they might adjust the payout.

I would just use a lawyer instead of my insurance company, but different strokes for different folks, I guess. By the way, since the other party is at fault, you might want to ask State Farm claims about transportation replacement and if they can offer you a rental car.

When I insured my Evo they said book price was 24k, my

Insur comp is suppose to be for enthusiasts, so I said this is a collectable and worth 34k how much to insure it for that agreed value, they said 200 a year more, so I said yeh put me down, when it came up for renew they listed agreed as 30k and I suppose hoped I just send off the check, but I called them and said hey WTF we had a deal and the young guy said sorry and put it back up to 34k.

Sorry OP to see this happen to you,everything covered above also if you're planning on buying back the wreck which is what I'd do, follow where it's gone and make sure it's under cover or go buy a tarp and cover it yourself, take pics of all your accessaries to as they may get stolen in the yard, if you don't care don't worry.

Glad you are OK! From the looks of where you two met, things could have been ALOT worse! Is it worth you buying it back, and either parting it out, or saving some parts for the next one? Is it at all worth rebuilding it? I know that the air bags were deployed, but? Regardless, best of luck! Sorry to see another one gone! RIP.

Most insurance look at actual market value of the car. They will look and see what cars similar to yours are be sold for in your area. The don't go off of blue book or NADA guides, as they do realize that those prices don't always reflect the market.

This sucks to see though. Your looks like it was really clean form looking at the undamaged panels

Most insurance look at actual market value of the car. They will look and see what cars similar to yours are be sold for in your area. The don't go off of blue book or NADA guides, as they do realize that those prices don't always reflect the market.

This sucks to see though. Your looks like it was really clean form looking at the undamaged panels

That's a relief. I couldn't find another BBY as immaculate as mine with low miles under 20k anywhere, so I'm hoping they factor that in. Took me 2 years to find this exact car. If the payout is nice, I'll probably buy a decent daily and go full race car with this one.

Payout should be nice and buy back should be cheap on this.

I would buy it back, remove the hood, windshield, bumper, fenders, radiator support, motor/transmission/transfer case and hollow out the engine bay so that there are no parts left. Then have it towed to your nearest frame straightener shop and have them pull it back into spec best they can. Then it's build time!

I like your idea of buying a daily and going full race with the evo. That's what I did last year after realizing how rare CT9A's are getting. We can never fully protect them, but we can increase the odds of keeping them safe.

By the way, since the other party is at fault, you might want to ask State Farm claims about transportation replacement and if they can offer you a rental car.

By the way, since the other party is at fault, you might want to ask State Farm claims about transportation replacement and if they can offer you a rental car.